Reporting is essential to any sustainability strategy. Your company might already be under pressure to prove its commitment to environmental sustainability, driven by regulatory requirements, growing consumer awareness, and investor demand.

Sustainability reporting is an ever-changing landscape in the European scenario. It refers to the practice of transparently communicating a company’s environmental, social, and governance (ESG) performance.

This article will explore the benefits and challenges of a mandatory regulation affecting sustainability reporting – the Corporate Sustainability Reporting Directive (CSRD).

What is CSRD?

CSRD is an EU legislation, effective from 5 January 2023, that enhances transparency by requiring businesses operating within the EU to report social and environmental impact and how their environmental, social, and governance (ESG) actions affect their business.

CSRD Synopsys

- Modernises and strengthens the rigour of environmental and social information that companies operating within the EU must report by expanding on theNon-financial Reporting Directive (NFRD).

- Broadens the scope by considering more companies

- Requires disclosure on a broader variety of sustainability problems and their effect on financial performance.

These standards will apply to:

- Large EU companies that meet at least two requirements: 40 million euros net turnover / 20 million balance sheet/ 250 employees

- Listed EU companies, including SMEs (except certain micro-enterprises that do not exceed two of the following three criteria including EU and non-EU subsidiaries): 10 employees / net revenue of EUR 700,000 / total assets of EUR 350,000.

- Non-EU companies with a combined group turnover in the EU of more than 150 million euros

The new reporting rules require companies to report sustainability-related topics covering a full range of environmental, social, and governance issues (including climate change, biodiversity and human rights), aiming to:

– Provide the investors and stakeholders with vital information to assess the company’s financial risks and opportunities arising from environmental issues.

– Improve transparency about the company’s impact on people and the environment.

The report on sustainability matters must be based on the double materiality principle, requiring companies to assess and report two dimensions of materiality: impact and financial. Actual or potential, positive or negative impacts on people or the environment over the short-, medium- or long-term are considered material.

When performing its materiality assessment, the company shall consider the provided list of sustainability matters covered in the European Sustainability Reporting Standards (ESRS), adopted by the Commission on July 2023, that specifies the sustainability information that companies subject to the CSRD shall disclose. These standards shall apply from 1 January 2024 for financial years beginning on or after 1 January 2024 for reports published in 2025 (see the ‘Timeframe’ section for further details about companies covered).

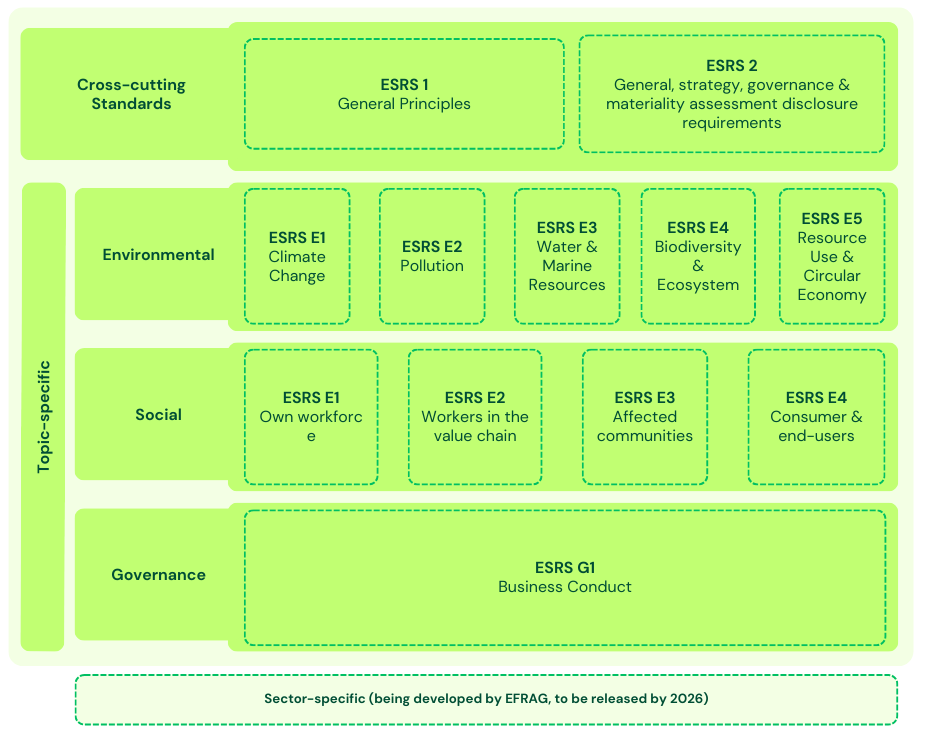

Below, Figure 1 illustrates the report requirements demanded by ESRS:

ESRS 2 (“General, strategy, governance & materiality assessment disclosure requirements”) specifies essential information to be disclosed and is mandatory for all companies under the CSRD scope. All the other standards are subject to materiality assessment, meaning that companies shall only report relevant information and omit information that is not material for its business model and activity.

The ESRS requires companies under the CSRD scope to perform a robust materiality assessment to ensure that all necessary sustainability information required is disclosed. If a company concludes that a topic is not material for its activity, a detailed explanation must be given. For example:

“If a company concludes that climate change is not a material topic and therefore does not report in accordance with that standard, it has to provide a detailed explanation of the conclusions of its materiality assessment with regard to climate change.”

Source: European Comission 2023

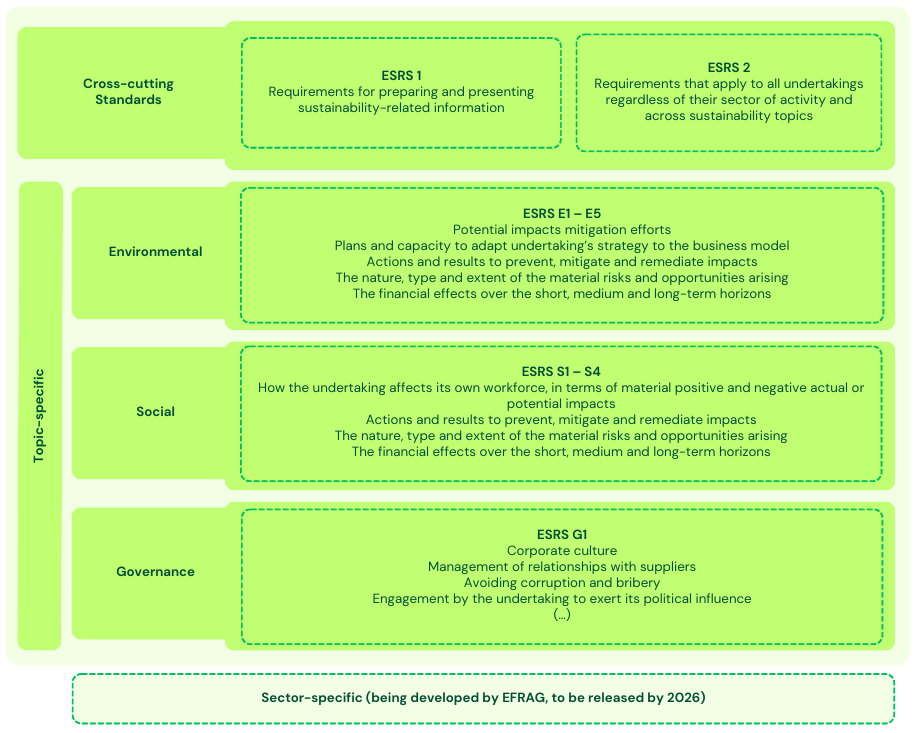

Figure 2 shows a summary of the objectives required for each standard:

Timeframe

What are the challenges of CSRD?

- Data collection and management

Data availability, accuracy, and reliability: Obtaining reliable and accurate data from different actors across the value chain (e.g., suppliers)

Data verification: CSRD mandates external verification by an independent third-party auditor. Ideally, ESG data must be controlled and validated internally to ensure transparency and auditability.

Data storage: Storing data and making it readily available.

- Assure compliance

Limited Assurance Expertise: Finding qualified auditors with the necessary expertise in sustainability and ESG issues

Cost: The cost of obtaining external assurance for sustainability report.

- Resource-intensive

Internal: Staff, time, and technology

Financial: To meet the requirements, companies may need to invest in new technologies, training, and consulting services.

Where to start with sustainability reporting?

1. Understand CSRD obligations

Start by identifying what needs to be reported under the scope of CSRD and determining the data required for reporting.

2. Conduct Life Cycle Assessment

A life Cycle Assessment will help identify material topics and generate accurate data for reporting.

3. Collaborate with suppliers

Early collaboration with suppliers is crucial to collecting all relevant data within your supply chain needed for reporting.

4. Centralise data

A centralised data system ensures that all data is organised and accessible for reporting or readily available for verification.

5. Align CSRD and business operations

Sustainability integration into the business system as a strategic move. This might involve modifying existing systems to accommodate sustainability reporting and training staff to ensure all departments know their role in CSRD compliance.

How data-driven software can help with reporting?

Effective data collection and management are the backbone of CSRD compliance. Susplus offers a solution to gather and assess your data promptly to help companies overcome sustainability reporting challenges, such as CSRD. It acts like a central hub to collect data from different sources, automate data entry and analysis, and inform decision-making on sustainability initiatives.

Our data-driven software supports companies of all sizes in measuring their products’ impact, creating action plans, reporting in compliance with standards, and compensating for the impacts the business is unable to avoid.

References

European Comission (2023). Questions and Answers on the Adoption of European Sustainability Reporting Standards. Available: https://ec.europa.eu/commission/presscorner/detail/en/qanda_23_4043 [Acessed: December 2024]

Greenomy (2023) The European Sustainability Reporting Standards: a Phase-in Journey to Sustainability Alignment. Available: https://www.greenomy.io/blog/esrs-phase-in-journey [Acessed: December 2024]

KPMG (2022) Get ready for European Sustainability Reporting Standards. Available: https://assets.kpmg.com/content/dam/kpmgsites/xx/pdf/ifrg/2024/talkbook-get-ready-for-esrs.pdf [Acessed: December 2024]

About Susplus

Susplus offers a simple, intuitive, and innovative data-driven platform service that supports companies of all sizes to accelerate their path transition to carbon neutrality. We empower companies to start and accelerate their carbon neutrality transition process by measuring and improving their business ecosystem value-chain impact. Susplus platform’s innovative features and intuitive design, will lead you during the transition journey by helping your team to measure carbon emissions in your business value-chain, create action-plans to easily reduce them, and report confidently in compliance with the latest reporting standards. Learn more at susplus.tech, on Linkedin, and on X @susplustech